%20(1).png?width=1200&height=628&name=June%203%20-%20Statement%20of%20account_%20Free%20downloadable%20template%20(PDF%2c%20Excel%2c%20%26%20Word)%20(1).png)

Need a clear and professional statement of account for your business? Whether you're prompting payment or providing a transaction summary, getting it right matters more than most businesses realise.

According to Chaser's 2026 The accounts receivable report, 40% of businesses spend six or more hours per week on accounts receivable tasks. A well-structured statement of account won't eliminate that burden on its own, but it's one of the clearest ways to reduce unnecessary back-and-forth, disputes, and delays before they start.

This guide provides a free, downloadable statement of account template (Excel), explains every component, shows you how to customize them, and covers best practices to ensure you’re set up for success.

Free statement of account template download (Excel)

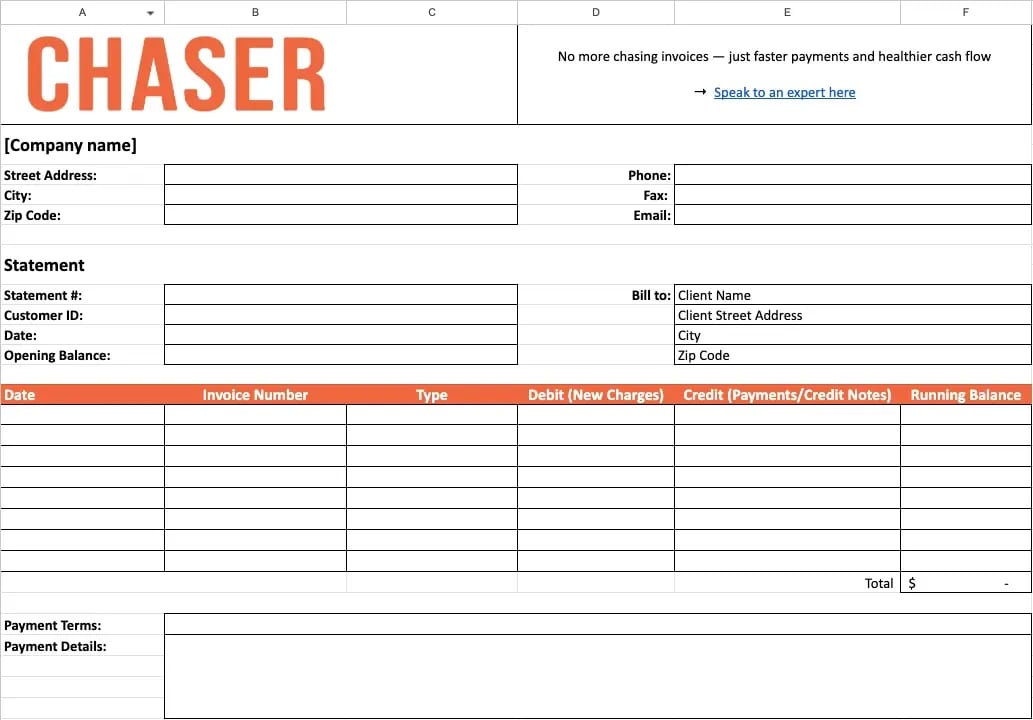

Streamline your accounts receivable with Chaser’s free, customizable Statement of Account template in Excel. This template helps you communicate outstanding balances, encouraging faster payments and healthier cash flow.

It's easy to use and includes all the essential fields for professional statements. You can brand it with your logo and company details, ensuring a consistent and professional image.

Our template also features separate tabs for different currencies, simplifying international transactions. Once downloaded, you can easily save it in any format you prefer, such as PDF, for seamless sharing.

Ready to simplify your billing?

→ Download your free statement of account template here.

Statement of account copy and paste email templates

The way you send a statement of account matters as much as the document itself. Below are two ready-to-use email templates you can adapt for your business.

Template 1: Standard monthly statement

|

Subject: Your statement of account for [Month] – [Your Company Name] Dear [Client Name], Please find attached your statement of account for the period ending [date]. Your current balance is [amount]. If you have already arranged payment, please disregard this notice. If you have any questions about the transactions listed, please do not hesitate to get in touch. Kind regards, [Your Name], [Your Company Name] |

Template 2: Overdue balance statement

|

Subject: Outstanding balance – Statement of account for [Client Name] Dear [Client Name], I hope this message finds you well. I am writing to draw your attention to an outstanding balance on your account. Please find attached your updated statement of account, which shows an overdue amount of [amount] relating to invoice(s) [invoice numbers]. We would appreciate payment at your earliest convenience. If there is a query or dispute regarding any of the invoices listed, please contact us so we can resolve this promptly. Thank you for your continued business. Kind regards, [Your Name], [Your Company Name] |

What happens after you send a statement of account?

A statement of account is the starting point for your follow-up. Most businesses send a statement and wait, but having a clear plan for what happens next is what separates businesses with healthy cash flow from those with growing debtor lists. Here is how a structured accounts receivable follow-up sequence works after a statement goes out.

Step 1: Payment received: Reconcile and close

Businesses that follow up on 100% of their overdue invoices are 76% more likely to be paid within one week than those that leave invoices uncontacted.

If the client pays promptly after receiving the statement, record the payment against the relevant invoices, update your accounts receivable ledger, and issue a remittance confirmation if appropriate. This closes the loop and keeps your records accurate.

Step 2: No response after 7 days: Send a follow-up reminder

If you have not received payment or acknowledgement within a week of sending the statement, send a polite follow-up email referencing the statement. Keep the tone professional and assume it may have been overlooked. Include the total outstanding balance and a clear link or attachment to the original statement.

Step 3: No response after 14 days: Escalate to a phone call

If there is still no response after two weeks, escalate to a direct phone call. Have the statement and the specific invoice numbers to hand before you call. The goal is to confirm receipt of the statement, identify any disputes, and agree on a payment date. Document the outcome of the call in your records.

Step 4: 30+ days overdue: Issue a formal demand

If the balance remains unpaid beyond 30 days with no agreed resolution, consider issuing a formal letter of demand. This sets out the outstanding amount, the invoices involved, and a final deadline for payment before further action is taken. At this stage, you may also wish to pause credit terms for the client until the balance is settled.

Step 5: Escalate to collections if necessary

If payment is still not received after a formal demand, the next step is to engage a collections agency or take legal action. This is a last resort, and maintaining clear records of all communications, including the original statement, follow-up emails, call logs, and the demand letter — will be essential if the matter proceeds further.

Automate the sequence so nothing falls through the gaps

Following up manually on every statement is time-consuming and easy to let slip, especially when you have multiple clients at different stages of the sequence.

Chaser automates this entire process: from sending the initial statement to triggering follow-up reminders at the right intervals, tracking client responses, and escalating overdue accounts.

This means your AR team spends time on exceptions and relationships, not on chasing every individual invoice.

What is a statement of account?

A statement of account is a summary of transactions between a seller and a buyer over a specific period.

Purpose for businesses:

- Payment reminder/gentle nudge: It serves as a prompt for clients to pay outstanding amounts.

- Provides a clear transaction history for both parties: An organized statement offers a detailed history of previous transactions.

- Helps in reconciling accounts: It’s beneficial for both parties to ensure that records are consistent.

- Can be part of the debt recovery process: A well-prepared statement can assist in recovering overdue payments.

Is a statement of account the same as an invoice?

No, a statement of account and an invoice serve different purposes. An invoice is a request for payment for a specific transaction, while a statement of account provides a comprehensive overview of all transactions during a certain period, including invoices, payments received, and outstanding balances.

Statements of account contain the following:

- A summary of all transactions

- The statement period (the specific period in which it applies, such as the month or quarter)

- A reference number for identifying the statement

- The customer's name and account number

- Your business name

- A list of transactions with dates

- A reference to the original invoices or purchase orders

- The new balance and total balance in the current period

- Past due amount, if any

- The date the statement was prepared

- Credit notes usually represented as a negative value

By contrast, an invoice simply summarizes all the transaction information for one particular sale transaction affecting the customer. For example, one service that is purchased, or one order of goods from a business.

An invoice contains the following:

- A request for payment

- The name, address, and contact information of the person or company billing

- A description of the goods or services provided

- The date(s) services were performed

- The amount due for each line item

- Terms of payment (due date, discount percentage for early payment)

- Any other relevant information about the transaction including late payment fees

Statement of account vs billing statement

The terms are often used interchangeably, but there is a subtle difference depending on context. A billing statement typically refers to a document that summarises charges and payments for a specific billing cycle, often used by businesses that bill on a recurring or subscription basis. A statement of account is broader: it covers all transactions between a seller and a buyer over a period, including invoices issued, payments received, credits applied, and any outstanding balance. In practice, both documents serve the same core purpose to keep both parties aligned on what has been billed and what remains unpaid.

What does SOA stand for?

SOA stands for Statement of Account. The abbreviation is widely used in accounts receivable, particularly in business-to-business contexts. You may see it referenced in accounting software, email subject lines, and payment correspondence. An SOA and a statement of account are the same document.

Why statements of account matter

92% of businesses report their invoices are typically paid after the due date, with 17% waiting more than 30 days. So, being proactive with sending statements of account can help bring in payments faster among other benefits like;

- Improved cash flow:

- Encourages prompt payments: Clear statements detail balances, due dates, and services, leading to faster payments.

- Facilitates easier reconciliation: Detailed statements help clients reconcile charges with their records, reducing disputes.

- Reduced queries:

- Self-service information for clients: Statements provide information on services, costs, and payment status, answering client questions.

- Minimizes communication overhead: Clients finding information on statements reduce calls and emails.

- Faster issue resolution: Detailed statements help resolve queries and discrepancies efficiently.

- Professional image for the business:

- Enhances credibility and trust: Professional statements demonstrate attention to detail and clear communication.

- Reflects efficiency and organization: Clear statements project an image of efficiency and professionalism.

- Supports positive client relations: Transparent financial information shows respect and builds stronger relationships.

Understanding time buckets

A "time bucket" is a strategic approach for organizing outstanding invoices according to how long they've been overdue. This method is especially advantageous for managing accounts receivable because it enhances:

- Debt Visibility: Enables businesses to clearly see which debts need immediate action.

- Priority setting for follow-ups: Helps concentrate efforts on invoices that are the most overdue.

- Payment behavior analysis: Assists in spotting trends, identifying customers who pay promptly versus those who delay.

- Organizing invoices into time-specific categories allows businesses to manage collections effectively and maintain a transparent view of their financial standing.

Examples of time buckets

- 0-30 days overdue: Invoice #1023 for $1,500 USD and Invoice #1027 for $2,200 USD needing early reminders.

- 31-60 days overdue: Invoice #1015 for $3,750 USD and Invoice #1019 for $4,500 USD requiring urgent follow-ups.

- 61-90 days overdue: Invoice #1009 for $5,600 USD and Invoice #1012 for $2,900 USD needing critical attention.

- Over 90 days overdue: Invoice #1001 for $8,300 USD and Invoice #1004 for $7,100 USD might require escalated collection efforts.

By systematically placing invoices into these categories, businesses ensure a more effective approach to managing overdue accounts.

Group by number of days they’re overdue

One of the most common methods to create time buckets is by categorizing overdue invoices based on the number of days they have been outstanding. This approach typically breaks down overdue accounts into intervals such as:

- 0-30 days overdue: Invoices that have just missed the due date and may still have a relatively high chance of collection with gentle reminders.

Example: Invoice #1032 for $1,250 USD and Invoice #1034 for $3,100 USD require immediate yet gentle follow-ups. - 31-60 days overdue: Accounts that are starting to become concerning and may require more assertive follow-up strategies.

Example: Invoice #1025 for $4,500 USD and Invoice #1029 for $2,800 USD are in need of determined follow-up efforts. - 61+ days overdue: Invoices that are significantly overdue and may involve a more formal collection process.

Example: Invoice #1011 for $6,750 USD and Invoice #1016 for $5,200 USD may demand an escalated approach to collections.

By structuring the overdue accounts into these categories, businesses can efficiently target their collection efforts, improve cash flow management, and reduce the risk of bad debts.

Group by issue date

Another way to use time buckets is by grouping invoices based on their issue date. This approach provides a clear chronological view of your accounts receivable, making it easy to assess payment timelines. By listing invoices from the oldest to the newest, businesses can quickly spot overdue invoices and prioritize which ones need immediate attention. Here’s an example of how to categorize invoices using their issue dates:

- Invoice #1032 for $1,250 USD, issued 1-30 days ago: Recent transactions that may still have time for payment.

- Invoice #1025 for $4,500 USD, issued 31-60 days ago: Invoices that are past due but not excessively so, warranting reminders.

- Invoice #1011 for $6,750 USD, issued over 60 days ago: Invoices that require urgent attention and possibly escalation to a formal collections process.

Using the issue date as a time bucket helps you track the duration since the sale occurred, enabling you to address collections more strategically based on how long each invoice has awaited payment.

Group by closing date and due date

A third approach for using time buckets involves grouping invoices according to their closing date or due date. This method is particularly helpful when preparing year-end statements or reports, allowing businesses to manage their accounts effectively.

- Closing date grouping: You could categorize transactions based on the closing date from the most recent to the oldest. This approach is ideal for assessing payment trends and cash flow over specific periods.

- Due date grouping: Invoices can also be sorted by their original due dates, allowing you to quickly identify upcoming payment deadlines. For instance:

- Invoices that are due this week

- Invoices that are due in the next month

- Invoices that have passed their due dates

By grouping invoices in this way, you can build a clearer picture of imminent cash flow and manage expectations more accurately. It also assists in prioritizing follow-ups to ensure that debts are settled before they enter the next overdue category.

What to include in a statement of account

Your statement of account needs these key components:

- Your business details: Name, address, contact information, and VAT registration if applicable.

- Client's business/customer details: Name and address of the client.

- Statement date: The date you issue the statement.

- Account number/customer ID: To identify transactions uniquely.

- Period covered by the statement: For example, "For the period 1 May 2025 to 31 May 2025."

- Opening balance: Clearly stating if it carries over from a previous period.

- Chronological list of transactions:

- Date of transaction

- Invoice numbers (hyperlinked if digital)

- Brief description of goods/services (optional, or refer to the invoice)

- Payments received (clearly marked)

- Credit notes issued/applied

- Debits (new invoices)

- Running balance: Optional, but helpful for clarity.

- Closing balance/amount due: Total outstanding amount.

- Payment terms: e.g., "Payment due within 14 days of this statement."

- How to pay: Include bank details, online payment links, and any other payment methods.

- Contact information for queries: Make it easy for clients to reach you with any questions.

How to customize and use your statement of account

Designing a clear and professional statement of account is crucial for fostering strong client relationships and securing prompt payments. Personalization not only showcases professionalism but also adapts the document to meet the unique requirements of your business and its clients. Follow this step-by-step guide to successfully tailor and use your statement of account:

Step 1: Choose the most relevant sample

Start by choosing a statement of account template that fits your business requirements and transaction types. Numerous templates are available, tailored to specific situations, such as services provided, goods sold, or credit notes issued. Make sure the template you select covers all the essential elements typically involved in your business transactions.

Step 2: Add your company logo and branding

Enhancing your statement with branding elevates its professional look and strengthens your business image. Place your company logo prominently at the top and consistently apply your brand colors and fonts across the document. This approach not only ensures recognizability but also signals to clients that professionalism is a core value of your business.

Step 3: Accurately fill in your business and client details

Fill in the document with precise details. Include your company's name, address, contact information, and VAT registration number if needed. Verify the client's information is accurate, ensuring their name, address, and related account identifiers are correct. Such meticulousness prevents misunderstandings and ensures clarity from the beginning.

Step 4: Double-check all transaction dates, invoice numbers, and amounts

Accuracy is paramount in financial documentation. Prior to completing the statement, carefully verify all transaction dates, invoice identifiers, and payment figures. Mistakes in these details can result in disagreements and diminish trust. Maintaining consistent precision in reporting instills confidence in clients and fosters solid business relationships.

Step 5: Ensure opening and closing balances are correct

Begin by clearly displaying the opening balance at the top of the statement, indicating whether it has been carried over from the prior period. Ensure that the closing balance accurately reflects all transactions, showing the current total amount due. Cross-check these balances against your accounting records to prevent any discrepancies.

Step 6: State payment terms and methods

Clearly outline payment terms in your statement, like "Payment is due within 14 days from the date of this statement." Specify the accepted payment methods, such as bank transfer details, an online payment link, or other available options. Offering clear instructions streamlines the payment process for clients, enhancing the chances of receiving payments promptly.

Step 7: Save with a clear file name

When saving the document, choose a clear and descriptive file name for easy retrieval. A suggested format might be “[YourCompanyName]-Statement-[ClientName]-[Date].pdf.” This naming strategy helps maintain organized and accessible records, effectively streamlining your accounts receivable management.

Step 8: Maintain professionalism throughout the document

The content and tone you use in client communications are crucial. Always employ professional and courteous language in the statement. Ensure that descriptions are clear, avoiding any jargon that might confuse clients. The statement should demonstrate a keen awareness of your client's needs while consistently maintaining a professional tone.

Step 9: Distribute your statement of account effectively

Give thoughtful attention to the method of distributing your statement of account. Opt for the PDF format, as it is non-editable and thus maintains the document's integrity. Deliver the statement through email, using a professional subject line such as “Statement of Account from [Your Company Name] for [Client Name].” Include a concise and polite message in the email to reiterate the statement's key details.

Step 10: Encourage feedback and communication

Ultimately, it's beneficial to add a note inviting clients to contact you with any questions or concerns. Clearly provide your contact details to highlight your openness to communication. This strategy can cultivate trust and nurture a strong, positive relationship with your clients.

When to send a statement of account to customers

Sending a statement of account is an important communication step in managing accounts receivable. Implementing best practices can improve clarity, reinforce professionalism, and ultimately lead to faster payments.

Here are some key strategies to consider when sending a statement of account to your customers:

- Regularly (e.g., monthly for active accounts)

Sending statements monthly helps maintain communication and keeps clients informed of their financial standing with your business. Regular updates can serve as reminders for due amounts and upcoming deadlines, fostering a routine that encourages timely payments.

- When an account becomes overdue

Timing is crucial. If a payment is overdue, it’s vital to send the statement promptly, ideally within a few days of the due date. This approach serves as a gentle reminder, highlighting the outstanding amount and prompting clients to address the overdue balance before it escalates.

- Upon client request

Clients may reach out for a statement of account if they want to clarify a specific transaction or reconcile their records. Being responsive to such requests not only strengthens the relationship with your client but also demonstrates that you value their business and concerns.

How to send a statement of account

- Use PDF format for non-editable versions

When issuing a statement, opt for PDF format. This format is generally non-editable, ensuring that the document’s integrity is retained and preventing inadvertent alterations that could lead to confusion or disputes. - Craft a professional email subject line

The subject line should be clear and informative. For example, “Statement of Account from [Your Company Name] for [Client Name].” A concise subject helps clients quickly identify the nature of the email and what to expect, making them more likely to open and review it. - Write a brief, polite email body

Accompany the statement with a brief email that summarizes its contents. Politely remind the client of their outstanding balance and express gratitude for their business. A well-crafted email body conveys professionalism and maintains a positive tone. For example:

| Dear [Client's Name], I hope this message finds you well. Please find attached your statement of account for the period ending [date]. The total amount due is [amount]. Should you have any questions or require further details, please don't hesitate to reach out. Thank you for your continued support. Best regards, [Your Name] [Your Company Name] [Contact Information] |

- Consider read receipts or follow-up tools

Utilizing read receipts can help you track whether your client has opened the email, which can be useful in managing your follow-ups. If your clients consistently overlook statements or emails, consider using follow-up tools like Chaser, which can automate reminders and track engagement, allowing you to maintain effective lines of communication. - Keep copies of the statement

It is essential to keep a copy of every statement you send. Maintain digital or physical copies for your records, as they can serve as a reference in case of disputes or questions. Having a history of communications will help your team track outstanding debts and provide clarity during future discussions with clients.

Additional considerations for enhancing effectiveness

- Customize communications for individual clients

Tailor your statements to address specific client needs or preferences. If a client prefers receiving statements at the end of the month rather than weekly, make a note of this in your records. Personalizing communication builds trust and demonstrates that you value and respect their needs.

- Maintain a clear and consistent format

Consistency in the layout and design of your statements establishes a professional image and helps clients recognize your documents quickly. Ensure that all necessary information is easily accessible, using a clear font and logical arrangement, making it simple for clients to understand their current financial position.

- Follow up on overdue statements

If you don’t receive a response after sending a statement of account, follow up with a reminder email or a phone call. This can prompt action from clients who may have overlooked the statement. Persistence is key, but be sure to maintain a polite tone, as preserving the client relationship is prime. - Be proactive about clarifying payment terms

Make sure your payment terms and methods are clearly communicated within the statement. If any terms are ambiguous, clients may hesitate to make payments. Provide clear instructions and contact information should clients have questions or concerns about their outstanding balances.

Common mistakes to avoid when issuing statements of account

Here are some common pitfalls and their potential consequences:

- Incorrect opening balance: This can lead to client disputes and mistrust.

- Missing transactions or payments: Incomplete statements complicate reconciliation.

- Unclear descriptions or invoice references: Ambiguity can confuse clients and lead to delayed payments.

- Outdated client contact information: Sending statements to old addresses can mean missed communications.

- Vague payment terms or missing payment details: Lack of clarity can result in late payments.

- Sending to the wrong client: This can breach confidentiality and damage your reputation.

- Not following up on overdue statements: Neglecting reminders can lead to poor cash flow.

Save time by automating your account statements and letters

Handling a statement of account manually can lead to errors like incorrect data and lost documents, which may harm client relationships and disrupt cash flow.

Chaser solves these issues by automating the process, reducing mistakes, and ensuring that statements are always accurate and on time. This automation helps you avoid the pitfalls of managing data by hand and boosts the reliability of your financial communications, building trust and transparency with clients.

Chaser's user-friendly platform lets you easily customize templates and personalize messages, keeping your branding consistent and professional. This efficiency allows you to concentrate more on your main business projects instead of administrative tasks.

With Chaser, you save time and minimize stress, simplifying account management, improving cash flow, and enhancing client relationships.

Final thoughts

Clear and professional statements of account are essential for businesses striving to maintain healthy cash flow and robust client relationships.

These documents facilitate better understanding and resolutions around payments, enabling your business to get paid faster while minimizing confusion.

Download your preferred statement of account sample above and get started today.

Discover how Chaser can transform your accounts receivable processes by automating your statement of account communications. Say goodbye to manual data entry and hello to error-free, timely reminders and statements that keep your cash flow healthy.

Businesses using AR automation software are 52% more likely to be paid within two weeks than those relying on manual processes.

With Chaser, you can focus more on your business and less on chasing payments, ensuring you get paid faster while maintaining strong relationships with your clients. Speak to an expert to see how Chaser is different from your current solution.

FAQs

%20financing.png?width=400&height=225&name=What%20is%20accounts%20receivable%20(AR)%20financing.png)

%20(1).webp?width=400&height=225&name=Blog%203%20-%20Accounts%20receivable%20aging%20report_%20Your%20complete%20guide%20(+%20free%20template)%20(1).webp)