Chaser news & blog

Best 5 cash application software when your ERP isn't enough

A lump sum arrives with no remittance advice. Multiple customers have paid the same amount on identical...

Cash management automation: How to get accurate forecasts

Many finance teams continue to perform work that automation should be handling. Manual reconciliation,...

How to analyze accounts receivable and from customer payment behavior

Even after your best quarter on record, the bank balance is still lower than predicted.

Try these 5 software alternatives before you hire receivable management services

If you're searching for receivable management services, you're probably close to picking up the phone and...

FreshBooks users can now use the leading accounts receivable software

FreshBooks users can now benefit from the leading accounts receivable software, following Chaser's new...

Collecting £65,000 of debt for just £65

At a glance Chaser partner Trecelyn, provider of contracted FD services, saw their pilot client recover an...

Debt recovery during a pandemic: Available to all UK businesses

Debt collection is a complex and difficult process, especially if that’s not what you set your business up to...

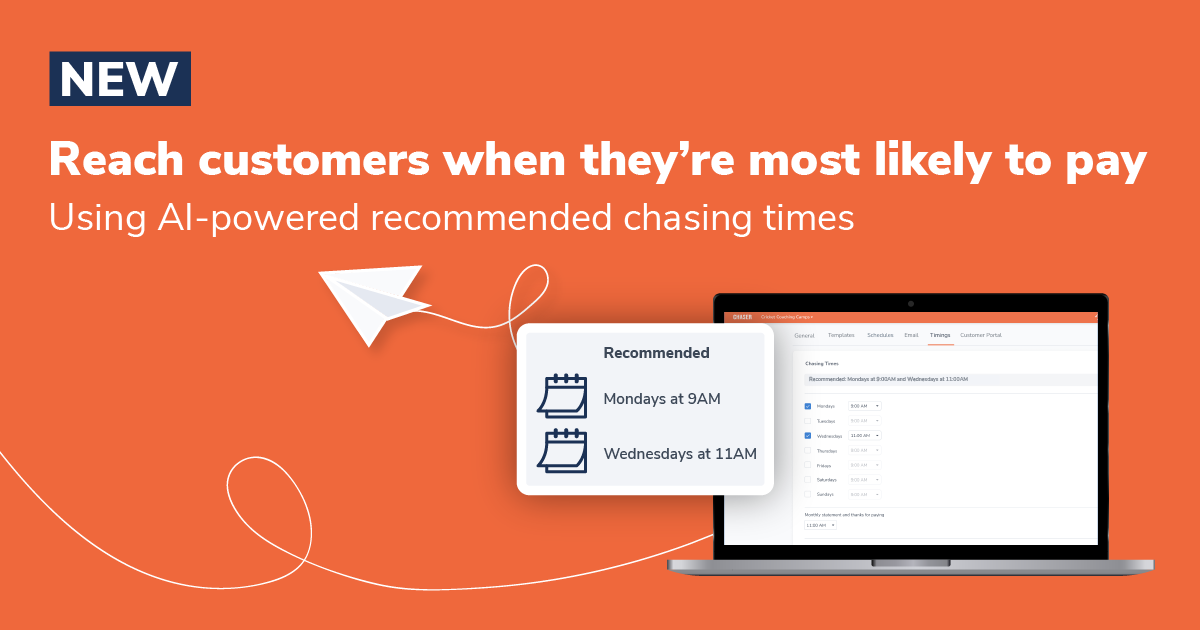

Reach customers when they're most likely to pay: recommended chasing times

Did you know that 50% of businesses spend more than four hours per week on accounts receivables tasks? This...

Debtor Daze is back for Xerocon 2019… with a twist!

It’s been nearly three years since we first collaborated with Anspach and Hobday to create the world's first...

How UHY Hacker Young overhauled their outsourced credit control

At a glance UHY Hacker Young is aTop 15 Groupof UK Chartered Accountants Their outsourced credit control...

How automation can improve efficiency with AccountsIQ and Chaser

Automation has become a business priority across several industries, with the Robotic Process Automation...

The role of payment portals in accounts receivable automation

Ensuring timely payments for products or services rendered can often be the most difficult part of running a...