Finance teams searching for accounts receivable outsourcing have typically found their current approach insufficient.

DSO has climbed the past 60 days and your cash flow is difficult to forecast while collections consume more hours every week.

Finance teams typically reach this point after attempting one of the following:

- Basic ERP automation sent reminders to customers who had already paid. It lacks the reconciliation logic to check payment status before chasing, which undermines credibility with clients.

- Offshore VAs introduced errors in payment matching and raised data security concerns around sharing customer financial data externally.

- Additional AR staff added headcount without fixing the workflows that caused the backlog in the first place.

- Outsourcing agencies offer a different kind of relief, but their fee structures, typically 25 to 50% of recoveries, make the total cost difficult to evaluate upfront.

Finance teams consider outsourcing only after these options appear exhausted, not as a first choice.

There's another option worth evaluating first. Intelligent accounts receivable automation solves the same core problems, manual workload, unreliable forecasting, and aging debt, while keeping customer communication internal and preserving visibility across the team.

This guide compares both approaches, outlines the trade-offs, and reviews six automation platforms to consider before outsourcing AR to an external agency.

Why do finance teams consider outsourcing accounts receivable?

Finance teams rarely search for outsourcing agencies when AR is running well. The search tends to happen when the current approach has become too costly, too time-consuming, or too unreliable to continue justifying.

When DSO starts compressing working capital

The clearest sign is usually a widening gap between receivables on the books and cash actually available. When Days Sales Outstanding climbs from the low 40s into the 50s or 60s, that gap starts locking up meaningful working capital. Every additional day represents cash sitting in outstanding invoices instead of funding operations.

When manual work outpaces the team's capacity

In many finance teams, AR workload grows faster than the team's ability to manage it. An AR manager works through spreadsheets, resends invoices, writes reminder emails, makes follow-up calls, and reconciles payments. Then the next batch of invoices moves into overdue status and the cycle repeats. When new overdue invoices arrive faster than the team can action them, the backlog grows regardless of effort.

When aged debt starts affecting revenue

AR problems that persist long enough stop being an efficiency issue. Bad debt climbs and invoices in the 90-day-plus bucket accumulate. When AR management becomes time-consuming or debt starts aging, some businesses look to outsourcing agencies as a way to reduce the internal workload. The appeal is less manual effort and a defined recovery process.

Why you should consider accounts receivable automation instead of outsourcing

Outsourcing reduces the team's workload and that’s an advantage.

When AR staff are overwhelmed with reminders, reconciliations, and follow-up calls, that reduction in workload is important. In some cases, particularly where there is no real AR infrastructure in place or where debt requires highly specialized handling, outsourcing can make sense.

But it should not be the default decision.

The relevant comparison is whether the same core problems can be solved without percentage-based fees or external handoff.

Intelligent AR automation is designed to address those same problems.

Cost: Fixed subscription vs percentage-based fees

An outsourcing agency may charge 25 to 50% of what it recovers, or a large monthly retainer. On a substantial recovered debt balance, that fee comes directly off the working capital improvement the business was trying to achieve. The more successful the recovery, the larger the amount paid out.

Automation works differently. The software cost is fixed based on platform scope and invoice volume, not on how much cash gets recovered. The more effective collections become, the more value the business retains.

For mid-market companies, the gap is often significant: the difference between a percentage-based fee that scales with recovery and a fixed subscription that does not.

Speed: Proactive prevention vs reactive recovery

Traditional agencies are usually engaged after debt has already aged badly. By the time an invoice reaches 90 days overdue, collection is harder, relationships are more strained, and the cash flow impact has already accumulated.

Intelligent automation starts earlier. It works before the due date, at the due date, and through the first stages of lateness, identifying risk earlier, sending reminders on better schedules, and removing payment friction before an invoice becomes a collections case.

One model responds after debt has become a problem. The other works to prevent invoices reaching that point in the first place.

Control: Visibility retained vs visibility surrendered

Outsourcing reduces direct oversight, which carries trade-offs.

Once you handoff collections, customer communication, tone, timing, and escalation are no longer fully controlled in-house. Reporting may be available, but it is rarely the same as having live visibility into what is being sent, which customers are responding, and what the next step is on each account.

Automation keeps that visibility internal. Reminders go out from the business's own email addresses, in its own voice. Communication history stays centralized. Accounting integration keeps invoice data current. Finance leaders can see what is happening without requesting updates from an external provider.

For businesses that care about cash flow and customer relationships equally, that visibility is not a secondary concern. It is central to how AR should operate.

Relationships: Professional persistence vs aggressive third-party collections tactics

Teams engage collection agencies because they will pursue accounts more persistently than an internal team is comfortable doing. The trade-off is that they become the face of the collections process, and their communication style may not reflect how the business wants to be represented to its customers.

When a long-standing customer account is transferred to a third party, the dynamic of that relationship can shift. For businesses where reputation and long-term trust are commercially important, that is a cost worth factoring into any outsourcing decision, separate from the fee itself.

Automation handles follow-up differently. Communication stays brand-aligned, the tone remains consistent, and payment can be made easier rather than more adversarial. That approach improves collection rates while keeping the customer relationship intact.

Intelligence: One-size-fits-all pressure vs AI-driven prioritization

Agencies rely on human judgment and manual prioritization. Basic software relies on static rules. Neither adapts well to the differences between customers.

Intelligent automation factors in payment history, timing patterns, customer segments, and real-time invoice status when deciding how and when to follow up. Reliable customers do not require the same treatment as chronically late ones. High-risk invoices should not wait for a monthly review to surface.

This is where modern AR platforms differ from the basic automation many finance teams have already tried. The difference is not simply that reminders are scheduled. It is that the scheduling, prioritization, and escalation logic are driven by data rather than fixed default rules. That addresses something outsourcing cannot: not a shortage of labour, but a lack of leverage over the process itself.

Summary comparison

Outsourcing replaces one manual process with another manual process managed externally. Automation removes much of the manual process entirely, and for most mid-market businesses, that is worth evaluating before committing to an agency.

Outsourcing vs AR automation platforms

Finance teams considering outsourcing are usually deciding between two very different models: handing AR work to an outside team or implementing software that automates the work while keeping control internally.

The table below shows how those models compare across the issues that actually drive DSO, working capital pressure, and customer experience.

|

Criteria |

Traditional outsourcing agencies |

Intelligent AR automation platforms |

|

Cost structure |

25-50% of collections or monthly retainer |

Fixed subscription based on volume and features |

|

Annual cost example for a $10M company recovering $500K |

Roughly $125K USD-$250K USD |

Often a fraction of that with fixed software spend |

|

Speed to impact |

Often 4-8 weeks for onboarding and handover |

Usually much faster once integrated and configured |

|

When they start working |

Commonly on aged debt, often 90+ days overdue |

Immediately, including pre-due reminders |

|

Control and visibility |

Lower visibility, external team handles outreach |

Full internal visibility through dashboards and audit trails |

|

Access to customer data |

Shared with third party |

Stays connected to internal systems |

|

Relationship impact |

Can be aggressive and damage trust |

Professional, brand-aligned, and easier to personalize |

|

Brand control |

Messaging handled by agency |

Messaging stays in-house |

|

Customer segmentation |

Often limited |

AI-driven segmentation and custom schedules |

|

Intelligence |

Human judgment, typically reactive |

Predictive models, payer insights, forecasting tools |

|

Payment infrastructure |

Usually none |

Payment portals, instant options, payment plans |

|

Cash flow forecasting |

Limited or none |

Often built into the platform |

|

Scalability |

Costs tend to rise with volume |

Scales more efficiently with automation |

|

When automation is not enough |

Agency is already the endpoint |

Some platforms include built-in escalation to collections specialists |

|

Best for |

Companies with no AR infrastructure or specialized debt situations |

Mid-market B2B teams that want faster payments, more control, and preserved relationships |

The comparison indicates that outsourcing provides relief, but at significant cost and with meaningful operational trade-offs. Automation can provide that same relief through systems rather than through agency labor, while preserving visibility and reducing cost dramatically.

That is why automation is the better first option to evaluate for most finance teams. The next step is choosing the right platform.

6 AR automation platforms to consider before you outsource

The comparison above illustrates why automation warrants evaluation before any outsourcing agreement is finalized.

The six tools below span a range of use cases, from enterprise-grade collections intelligence to mid-market platforms built to solve the exact problems that push finance leaders toward outsourcing. Each one has strengths and limitations.

The right choice depends on whether the priority is forecasting, customer experience, recurring billing, enterprise complexity, or the combination of prevention and escalation.

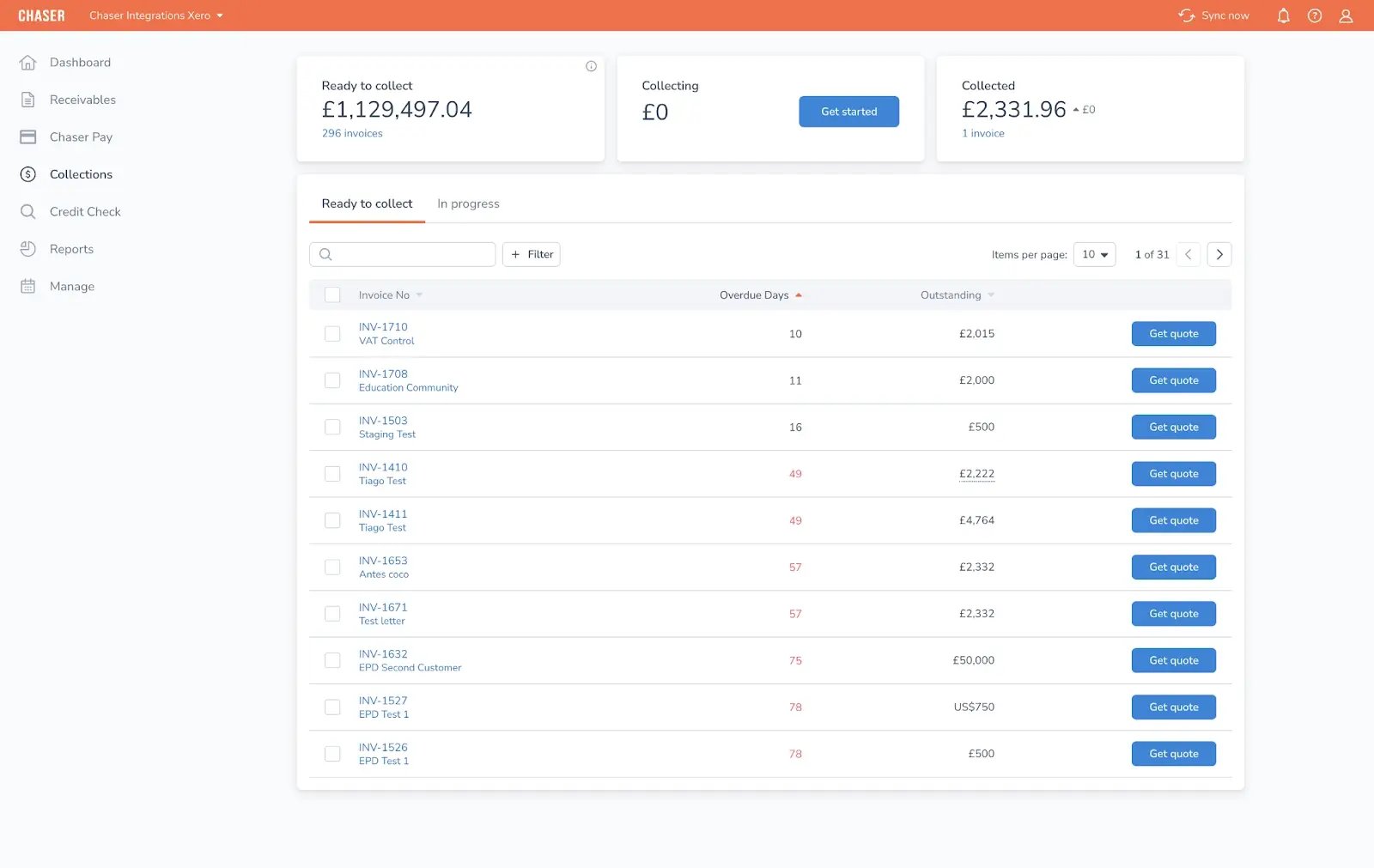

1. Chaser

Chaser is designed for finance teams experiencing possible conditions that typically prompt outsourcing consideration. These conditions include: when DSO is rising, collections work is consuming significant time, and the current mix of spreadsheets, basic reminders, and reactive chasing is no longer enough.

Instead of transferring the problem to an agency, Chaser automates the collections process proactively, keeps communications in the business's own voice, and combines that automation with cash flow intelligence.

This gives finance leaders visibility into not only which invoices are overdue, but when cash is likely to arrive based on how customers behave, not just what payment terms say they should do. Unlike most tools that handle either collections or cash flow forecasting, Chaser addresses both, and builds the forecast from the same payment data driving the collections engine.

When debt still needs specialist intervention, Chaser Collections provides an integrated escalation path without forcing a separate handoff to a traditional agency.

Chaser key features

- Automated multi-channel chasing across email, SMS, letters, and calls

- AI Late Payment Predictor for invoice-level payment risk

- Payment Portal with flexible payment options

- Revenue Forecast Tool for projected payment timing

- Payer Ratings for customer segmentation

- Two-way accounting integration with systems such as Xero, QuickBooks, Sage, Dynamics 365, and SAP

- Chaser Collections for specialist debt recovery when needed

What Chaser excels at

Chaser performs most effectively in scenarios where businesses require relief from manual collections without relinquishing internal control. The platform automates follow-up, payment reconciliation, and customer reminders in a way that is proactive rather than reactive. It does not wait for debt to age into a crisis.

Predict late payment and prevent aging debt

Late Payment Predictor and Payer Ratings help identify risky invoices before they move deeper into aging buckets. Revenue Forecasting improves visibility into when cash is likely to arrive, helping finance leaders make more informed decisions.

Follow up with customers through multiple channels

Chaser includes automated phone calls and voicemail as a standard channel. When emails go unanswered, the platform escalates to SMS, letters, and auto-call without any manual intervention. This multi-channel reach is most relevant when customer responsiveness declines.

Escalate collections beyond automation when you need to

Chaser Collections adds an escalation path inside the same ecosystem, solving one of the biggest practical objections to software-first AR. The collections team works collaboratively rather than through hard-line pressure, available on every plan, for individual invoices, on a no-win-no-fee basis. Around 80% of escalated cases resolve without legal action.

Businesses using Chaser often report getting paid faster prior to onboarding it. One case study reduced DSO from 60 days to around 24. Another recovered £800,000 in older debt through the integrated collections path.

Chaser pricing

Chaser offers tiered pricing based on company needs, features, and usage. The pricing page has more details on the different tiers for mid-market and enterprise businesses.

Chaser reviews

Chaser has a Capterra rating of 4.9/5 stars with recurring praise for time savings, faster collections, ease of use, and communication that stays professional.

For finance teams where collections workload and cash flow unpredictability are the primary drivers toward outsourcing, Chaser illustrates what intelligent automation can achieve as an alternative.

Finance teams use Chaser to recover aged debt. See how you can do the same with Chaser and improve collections before outsourcing to an agency.

2. ezyCollect

ezyCollect is a full-stack accounts receivable platform built primarily for the Australian and New Zealand market, combining collections automation with credit data powered by illion.

Where most AR tools treat credit risk as a separate concern, ezyCollect integrates it directly into the collections workflow, giving finance teams visibility into a customer's financial health before deciding how aggressively to chase.

The SimplyPaid portal handles payment collection and Installment arrangements in one place, and the platform connects to major accounting systems used across ANZ. For businesses operating in that market who want collections, credit risk, and payments under one roof, ezyCollect is one of the most complete options available.

Key features

- Automated multi-channel chasing across email, SMS, and paper letters

- SimplyPaid payment portal with Installment and payment plan support

- illion-powered credit data and credit risk monitoring

- Credit limits with automated alert notifications

- Dispute management and promise-to-pay tracking

- Integrations with Xero, MYOB, and other accounting platforms common in ANZ

- Call reminders for collector follow-up on priority accounts

What ezyCollect excels at

ezyCollect's clearest advantage is the combination of credit intelligence and collections in a single platform. Most tools in this space handle chasing well but leave credit risk monitoring to a separate product.

ezyCollect uses illion's credit data to give finance teams an early warning system. If a customer's financial position deteriorates, the platform flags it before the invoice becomes a problem rather than after it is already overdue.

The Installment and payment plan functionality built into SimplyPaid is also more developed than many comparable platforms. Customers can agree payment arrangements through the portal directly, reducing the manual back-and-forth that typically slows recovery on larger or disputed balances.

ezyCollect Pricing

ezyCollect does not publish standard pricing publicly. Pricing is tailored based on business size and requirements.

ezyCollect Reviews

ezyCollect holds a 5.0 rating on Capterra and strong scores on Trustpilot. Users consistently highlight the quality of automation, ease of integration with ANZ accounting software, and the tangible impact on cash flow. A recurring theme is how the platform reduces manual follow-up work without making customer communications feel impersonal — one reviewer noted it had saved the business from needing to hire additional staff to chase debtors.

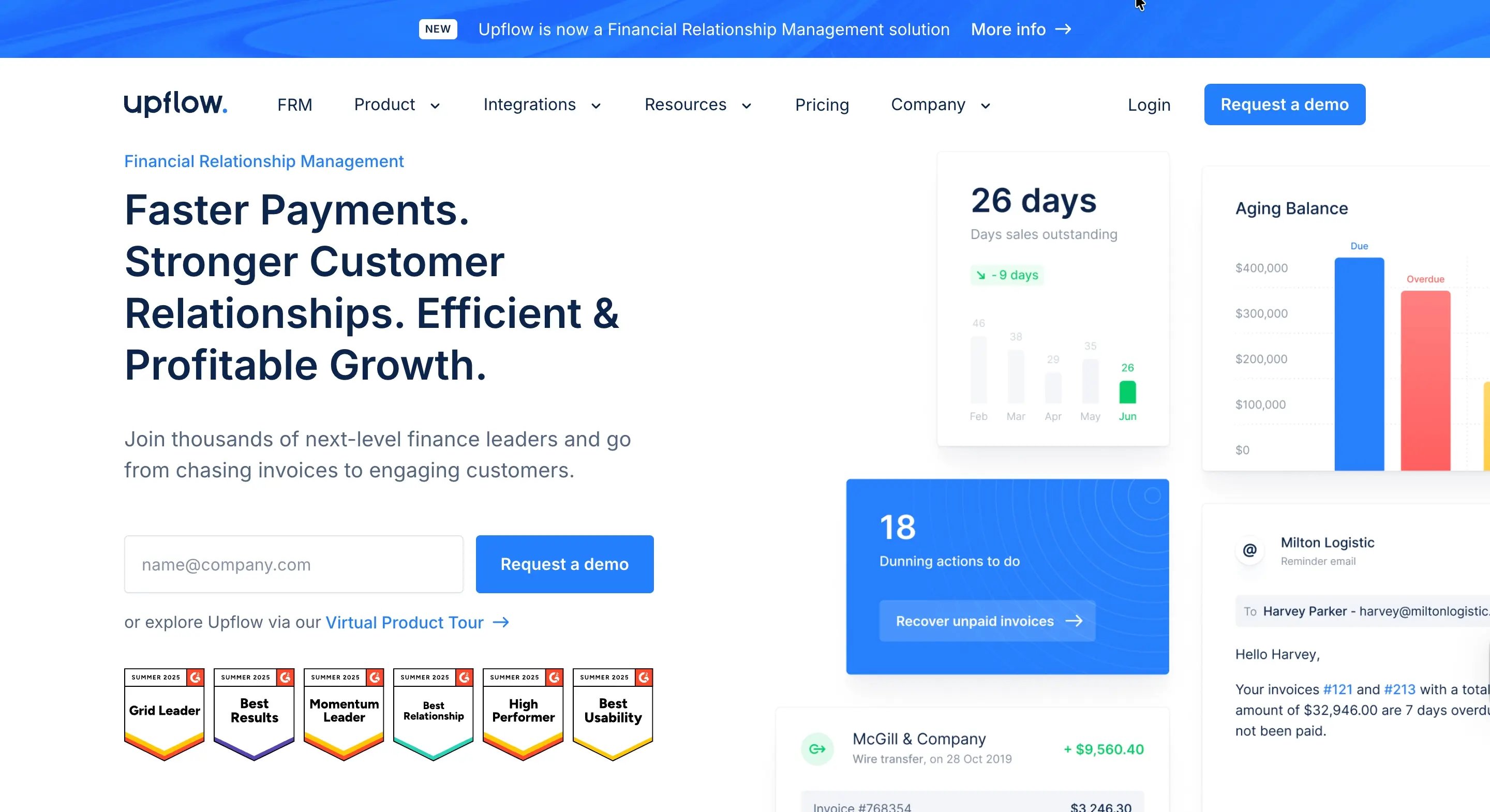

3. Upflow

Upflow positions itself as a Financial Relationship Management platform. The premise is that treating every overdue invoice identically risks damaging the customer relationships that drive repeat business. And that getting paid consistently well requires understanding payment behavior rather than just escalating pressure.

In practice, Upflow prioritizes customer segmentation, personalized communication campaigns, and a payment experience that feels frictionless rather than adversarial.

It is especially well-suited to growth-stage and mid-market B2B businesses that care as much about how they come across to customers as how quickly they collect and where the finance team needs to stay aligned with sales and customer success rather than operating in isolation.

If Upflow doesn't quite match what you're looking for, we've covered the best Upflow alternatives in a separate post to help you find a solution that better fits your needs.

Upflow key features

- Automated multi-channel reminder workflows across email, SMS, calls, and letters

- Branded customer payment portal with self-service invoice access

- Cash application and real-time ERP sync

- Team collaboration tools including @mentions and cross-functional visibility

- AI-driven insights including Promise to Pay tagging and customer payment behavior analysis

- Customer segmentation and Smart Rules for workflow personalization

- Financial forecasting and DSO/CEI dashboards

What Upflow excels at

Upflow's clearest strength is its usability. The interface is clean and quick to navigate, and the workflow setup is designed to get finance teams operational without a long implementation period. For teams coming off spreadsheets or a basic accounting system, the onboarding experience is notably lighter than most mid-market AR tools.

The payment portal reflects a similar emphasis on customer experience. It presents invoices clearly, makes the payment path obvious, and keeps the interaction professional without requiring the customer to chase down an invoice or go back and forth over email for payment details.

Upflow works best for teams that primarily need automated reminder sequences and a clean portal with relatively straightforward workflows. It handles standard dunning well, and the cash application feature matches payments without manual reconciliation.

Upflow pricing

Upflow offers a free Discover plan covering analytics and AR benchmarking, with no automation included. Paid plans unlock collections workflows and automation, and are priced on a quote basis.

Upflow reviews

Upflow has a rating of 4.5 on Capterra. Users often talk about its ease of use, the customer portal, and the amount of time saved compared with spreadsheets and manual follow-up.

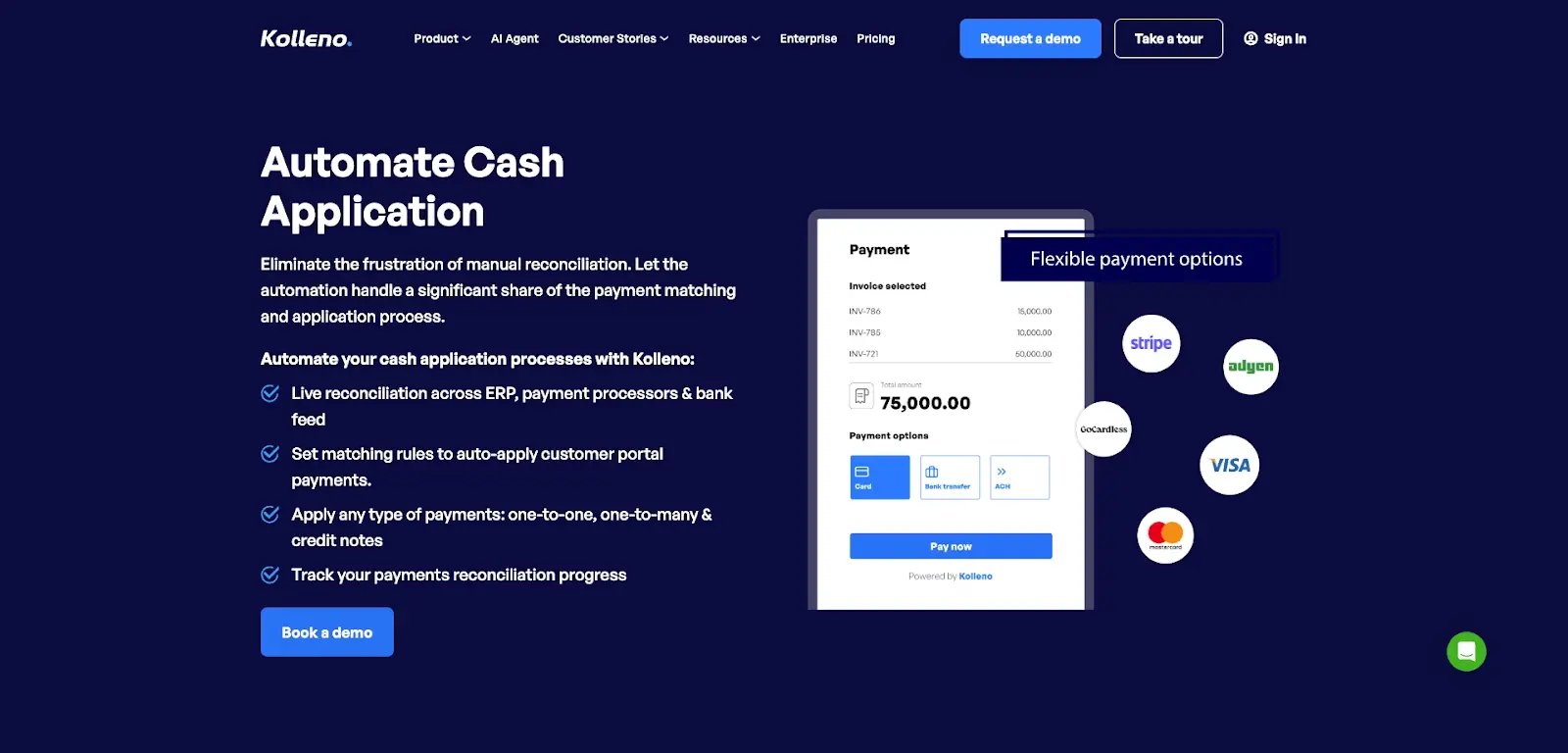

4. Kolleno

Most AR platforms are built around one core problem: chasing invoices. Kolleno is built around a different premise. Collections bottlenecks rarely come from one source, and solving them properly requires more than automated reminders.

Finance teams that struggle with DSO are often dealing with several disconnected problems at once: ERP data that does not sync in real time, disputes sitting unresolved in email threads, manual reconciliation consuming hours each week, and credit risk that only surfaces after an invoice has already aged.

Kolleno addresses all of that in a single platform. Collections, payments, dispute management, cash application, credit risk monitoring, and reconciliation are built and integrated in-house rather than assembled from separate tools. That distinguishes it from chasing platforms that have added adjacent features over time.

Kolleno key features

- Collections and AR workflow automation with drag-and-drop workflow builder

- AI Agents for automated follow-up, cash application, and payment prediction

- Automated cash application with real-time bank sync

- Credit risk monitoring with dynamic AI-driven credit scoring

- Dispute management and centralized communications workspace

- Collections task management with team delegation and escalation

- Customer payment portal with multiple payment methods

- Native integrations with NetSuite, Xero, QuickBooks, Sage, SAP, and MS Dynamics

What Kolleno excels at

Kolleno's clearest advantage is breadth combined with integration depth. Most AR platforms handle chasing well but leave reconciliation to another tool, credit risk to yet another, and dispute resolution to email. Kolleno pulls those functions into a single workspace.

The ERP sync runs every few minutes, not nightly, meaning invoice data, payment status, and dispute updates stay current rather than requiring manual imports or creating gaps between what the AR team sees and what is actually in the system.

It is suited to businesses who need more structured control over the full AR process, and grown beyond standard collections workflow.

Kolleno sits toward the larger end of the mid-market, where the breadth of functionality aligns with the complexity of the team's requirements. Teams with simpler AR workflows may find the feature set broader than their current needs.

Kolleno pricing

Pricing is quote-based.

Kolleno reviews

Kolleno holds a 5.0 rating on Capterra across 8 reviews. Users most consistently highlight the reduction in manual collections work and they point to task management and workflow automation as practical wins for teams managing complex credit policies with multiple steps.

5. Invoiced

Most AR platforms are built around one core problem: chasing invoices. Kolleno is built around a different premise. Collections bottlenecks rarely come from one source, and solving them properly requires more than automated reminders.

Finance teams that struggle with DSO are often dealing with several disconnected problems at once: ERP data that does not sync in real time, disputes sitting unresolved in email threads, manual reconciliation consuming hours each week, and credit risk that only surfaces after an invoice has already aged.

Kolleno addresses all of that in a single platform. Collections, payments, dispute management, cash application, credit risk monitoring, and reconciliation are built and integrated in-house rather than assembled from separate tools. That distinguishes it from chasing platforms that have added adjacent features over time.

Kolleno key features

- Collections and AR workflow automation with drag-and-drop workflow builder

- AI Agents for automated follow-up, cash application, and payment prediction

- Automated cash application with real-time bank sync

- Credit risk monitoring with dynamic AI-driven credit scoring

- Dispute management and centralised communications workspace

- Collections task management with team delegation and escalation

- Customer payment portal with multiple payment methods

- Native integrations with NetSuite, Xero, QuickBooks, Sage, SAP, and MS Dynamics

What Kolleno excels at

Kolleno's clearest advantage is breadth combined with integration depth. Most AR platforms handle chasing well but leave reconciliation to another tool, credit risk to yet another, and dispute resolution to email. Kolleno pulls those functions into a single workspace.

The ERP sync runs every few minutes, not nightly, meaning invoice data, payment status, and dispute updates stay current rather than requiring manual imports or creating gaps between what the AR team sees and what is actually in the system.

It suits businesses that have grown beyond basic chasing and need more structured control over the full AR process, not just which invoices are overdue, but why, and what is blocking resolution.

Kolleno sits toward the larger end of the mid-market, where the breadth of functionality aligns with the complexity of the team's requirements. Teams with simpler AR workflows may find the feature set broader than their current needs.

Kolleno pricing

Pricing is quote-based.

Kolleno reviews

Kolleno holds a 5.0 rating on Capterra across 8 reviews. Users most consistently highlight the reduction in manual collections work and they point to task management and workflow automation as practical wins for teams managing complex credit policies with multiple steps.

6. Gaviti

Gaviti is designed for larger B2B finance teams where collections is not a one-department activity. In many mid-market and enterprise environments, chasing a customer is not purely a finance decision. It involves sales context, relationship history, active disputes, and sometimes multiple stakeholders across functions.

Gaviti is built around that reality. Its AI-driven workflows and collaboration tools create shared visibility across teams, so finance is not making collections calls in isolation from the account managers who own the relationship.

For businesses where that cross-functional complexity is a genuine constraint, Gaviti addresses it more directly than most AR platforms.

Gaviti key features

- AI Assistant for behavioral insights, payment prediction, and workflow guidance

- Automated collections workflows with multi-step sequences triggered by invoice age, risk level, or amount across email and SMS

- Credit management with integrated credit agency data, automated credit reviews, and real-time limit monitoring

- Dispute tracking and management with structured, trackable workflows

- Automated cash application with real-time payment matching and reconciliation

- Customer self-service portal with zero-fee ACH payments, invoice access, and direct communication

What Gaviti excels at

Gaviti's core strength is collaboration and intelligent prioritization. When a high-value account becomes unresponsive, it is rarely a pure collections problem but often requires sales input, dispute resolution, or context from customer success before finance can move.

Gaviti creates a shared workspace for that kind of coordination, making it easier to escalate the right accounts, involve the right people, and keep the process moving without losing track of where each case stands.

The AI workflow builder makes it easier to customize collections processes as teams grow. Rather than applying a single chase schedule to every debtor, Gaviti uses behavioral data to inform how and when to follow up, prioritising effort rather than treating every overdue invoice with the same urgency.

One consideration for some teams: Gaviti's outreach covers email and SMS but does not include auto-call functionality natively, which may be a factor for teams that rely heavily on phone-based follow-up as part of their collections process.

Gaviti pricing

Gaviti uses quote-based pricing. Pricing scales with team size, invoice volume, and feature requirements.

Gaviti reviews

Gaviti has a rating of 4.5 from 91 reviews on Capterra. Users commonly praise the platform's workflow automation, AI-driven prioritization, and the way it improves collections coordination across departments.

Which AR automation should you try before you outsource?

The right platform depends on what problem needs solving first.

Choose Chaser if the business is dealing with immediate cash flow pressure, rising DSO, too much manual collections work, and a need to prevent invoices becoming late rather than simply reacting after they age. It is especially strong for mid-market B2B teams that want predictive intelligence, relationship-safe automation, and access to collections expertise when needed.

Choose ezyCollect if the business operates in Australia or New Zealand and wants collections automation combined with credit risk monitoring and Installment management under one roof.

Choose Upflow if customer experience is a major priority and the goal is to automate collections while making the payment journey feel smooth and professional — particularly for growth-stage and mid-market B2B businesses where preserving customer relationships matters as much as collecting faster.

Choose Kolleno if AR operations are broad and complex enough to require one platform covering collections, reconciliation, disputes, credit risk, and payments — and where the priority is eliminating the friction of managing those functions across separate tools.

Choose Invoiced if the business relies heavily on recurring billing, subscription structures, or flexible pricing models where billing complexity is as much of a challenge as collections.

Choose Gaviti if collections decisions depend on collaboration across departments — particularly where finance, sales, and customer success need shared visibility to resolve accounts and AI-driven prioritization matters more than multi-channel reach.

A better first step than outsourcing

If outsourcing is on the table because collections are taking too long, DSO is climbing, and cash flow feels harder to predict every quarter, evaluate automation first.

Agencies remain a valid option in specific circumstances because agencies transfer the workload externally at a cost; automation reduces the workload through process efficiency.

With automation, the business keeps more of the cash it collects, keeps more control over customer relationships, and gets more visibility into what is happening across receivables.

For most mid-market teams, that represents the more efficient starting point.

Chaser reflects that model directly. It addresses the same underlying problems earlier and more proactively, with lower cost and greater internal visibility.

Frequently asked questions about AR outsourcing vs. automation

%20-%20Cash%20collection%20formula.webp?width=400&height=225&name=Blog%204%20(Nov)%20-%20Cash%20collection%20formula.webp)