If you're searching for receivable management services, you're probably close to picking up the phone and hiring an agency. Before you do, it's worth spending five minutes answering one question: is an agency actually what your situation requires?

The answer depends almost entirely on how old the debt is and what's happened so far. Some situations genuinely call for an agency. Many don't, and agency contracts typically charge 25-50% of recovered amounts.

Is an agency the right call?

A simple decision framework

|

Tier |

Your situation |

Recommended solution |

|

Tier 1 |

DSO 15 to 90 days. Invoices are overdue but still recoverable. You want to maintain customer relationships. |

Software first. Automated multi-channel chasing recovers most debt at this stage without agency fees. |

|

Tier 2 |

DSO 90 to 120+ days. Aged debt is building. Customers are going silent. You still want a sensible, relationship-aware recovery path. |

Hybrid approach. You need more than reminders, but less than a full agency handoff. |

|

Tier 3 |

DSO 365+ days. The customer has refused to pay or is unreachable. The relationship is already over, or preserving it no longer matters. |

A debt collection agency or legal route is the right call |

If you're in Tier 3, an agency may genuinely be your best immediate option. That should be said plainly.

But there's still a second question worth asking: once that debt is recovered or written off, what prevents the next group of invoices reaching the same stage. That's where software matters even for businesses that need an agency today. It helps with prevention that turns a one-time recovery exercise into a lasting fix.

If you're in Tier 1 or Tier 2, software should almost certainly be your first move. The rest of this guide shows which platforms are built for recovery, not just prevention, and which one covers all three tiers if you want a single system that handles both. We evaluated these products based on how their functionalities fit into these three tiers.

The best accounts receivable management software to consider before getting an agency

The comparison below makes the market easier to scan.

|

Software |

Best for |

Tier coverage |

Integrated recovery service? |

|

Chaser |

Mid-market hybrid solution |

Tier 1 + 2 + 3 |

Yes, human led |

|

Highradius |

Enterprise scale ($500M+ revenue) |

Tier 1 + 2 + 3 |

Third-party only |

|

Paidnice |

Small businesses on Xero/QuickBooks |

Tier 1 |

No |

|

EzyCollect |

Wholesalers, construction, distributors |

Tier 1 + 3 |

Third-party only |

|

Payt |

European SMEs, pre-collection escalation |

Tier 1 + 2 (automated) |

No human layer |

1. Chaser

Best for: Mid-market companies looking for a hybrid approach to receivables management and debt collection without compromising on the personal touch in the communications with customers.

Chaser is the strongest match for this problem because it covers the full receivables cycle rather than just one phase of it. It automates early and mid-stage chasing, adds integrated human collections support when invoices become aged and difficult, and includes predictive tools that help stop the same problem from repeating.

Most software options in this category are Tier 1 only. They automate reminders, improve visibility, and reduce manual effort, but when customers become unresponsive, the business still has to decide whether to keep chasing internally or hand the debt to an agency.

Chaser fills that gap. It gives one system for chasing what is overdue, escalating the difficult accounts sensibly, and preventing future invoices from reaching the same stage.

Chaser collections: The middle ground between automation and agencies

At some point, a portion of debt stops responding to standard reminders. The account is aged, the customer has gone quiet, and internal chasing isn't moving it. This is where many businesses assume the only next step is to hand the file to a traditional agency.

Chaser collections is integrated into the same platform, which means invoices can be escalated in one click without a separate handover process. Quotes are transparent and upfront. The service runs on a no-win-no-fee basis, and it can handle relatively small invoices as well as larger debts.

The style of recovery matters too. Chaser collections is built around agreeable outcomes where possible, not aggressive pressure tactics. That makes it a far better fit for businesses that still care about reputation and future customer value.

It also keeps visibility in one place. Collector actions, letters, SMS messages, calls, and other communications remain visible within the Chaser account, so the team retains full oversight throughout the escalation process.

That keeps costs lower and gives the business more control over how recovery is handled. The results reflect that. Huttie recovered $19,000 in old debts that would otherwise have been written off and The Community Energy Scheme recovered £800,000 in debt that had effectively been treated as unrecoverable.

Multi-channel automated chasing that removes the manual effort

Manual collections rarely fail because the team doesn't care. They fail because the process depends on human consistency in an environment where people are already overloaded.

Chaser removes that dependency with automated reminders across email, SMS, auto-call, and postal letters. The process keeps moving even when the team is busy, understaffed, or pulled into higher-priority work. Follow-up schedules escalate automatically, moving accounts from gentle reminders to firmer pressure without anyone manually managing every step.

If the debtor ignores emails, SMS or calls can bring the account back into motion. The pressure stays on overdue invoices while the team frees the team to focus on other priorities.

Chaser customers regularly report reclaiming 15 or more hours per week, and businesses such as Docuflow have seen payments arrive far faster after switching from manual collections.

Personalized reminders that still feel human

One of the biggest reasons teams hesitate to automate is fear of sounding robotic.

Generic reminder tools often create that exact problem because your messages get ignored because they feel impersonal, or they go out after payment has already been made and make the business look disorganized.

Chaser sends reminders from the company's own email address with the right signature and tone. Templates can be customized to match brand voice, and schedules can avoid weekends and public holidays so reminders arrive at times that feel considered rather than automated.

The key safeguard is real-time sync with accounting software. Paid invoices stop being chased as soon as the data updates, preventing the awkward situation where a customer is chased after they've already paid.

Payment Portal and Payment Plans that turn promises into cash

A lot of late payment friction is not outright refusal. It is delay, ambiguity, or inconvenience.

Customers say they will pay soon but never commit to a date. Others need flexibility but have no clean way to arrange it without creating more admin. In those situations, another reminder doesn't solve the real problem.

Chaser reduces that friction through Chaser Pay and the Payment Portal. Reminders can include direct payment links, and customers can pay by bank transfer, credit or debit card, Apple Pay, or Google Pay. They can also view outstanding invoices and download statements without contacting the business directly.

If a customer genuinely needs to spread payment, a structured payment plan is far better than another vague assurance. Chaser converts that conversation into something concrete and trackable, with installments chased automatically.

That turns a vague promise into a tracked commitment with automatic follow-up.

Chaser pros

- Covers all three tiers, from automation to hybrid recovery to collections escalation

- Saves meaningful manual time for AR teams

- Preserves customer relationships better than traditional agencies

- Keeps full visibility over communication and escalation activity

- Reduces the need for external agency handoff

- Adds a prevention layer through AI-driven risk signals

- Gives one platform instead of a mix of spreadsheets, reminders, and outside vendors

Chaser cons

- Not a replacement for legal action when the debt is very old and the customer has explicitly refused to pay

- Best suited to businesses with active receivables operations rather than companies with almost no invoicing activity

Pricing

Chaser offers tiered pricing depending on business needs and features. The best place to view current pricing is the pricing page directly.

Review

On Capterra, Chaser has a rating of 4.9 from 45 reviews. Users also regularly mention time savings, faster payments, more professional communication, and the feeling that collections have become manageable again rather than a persistent operational burden on the team every week.

Finance teams have recovered old debt using Chaser. See how Chaser can help you improve collections and do the same before outsourcing to a receivables management service company.

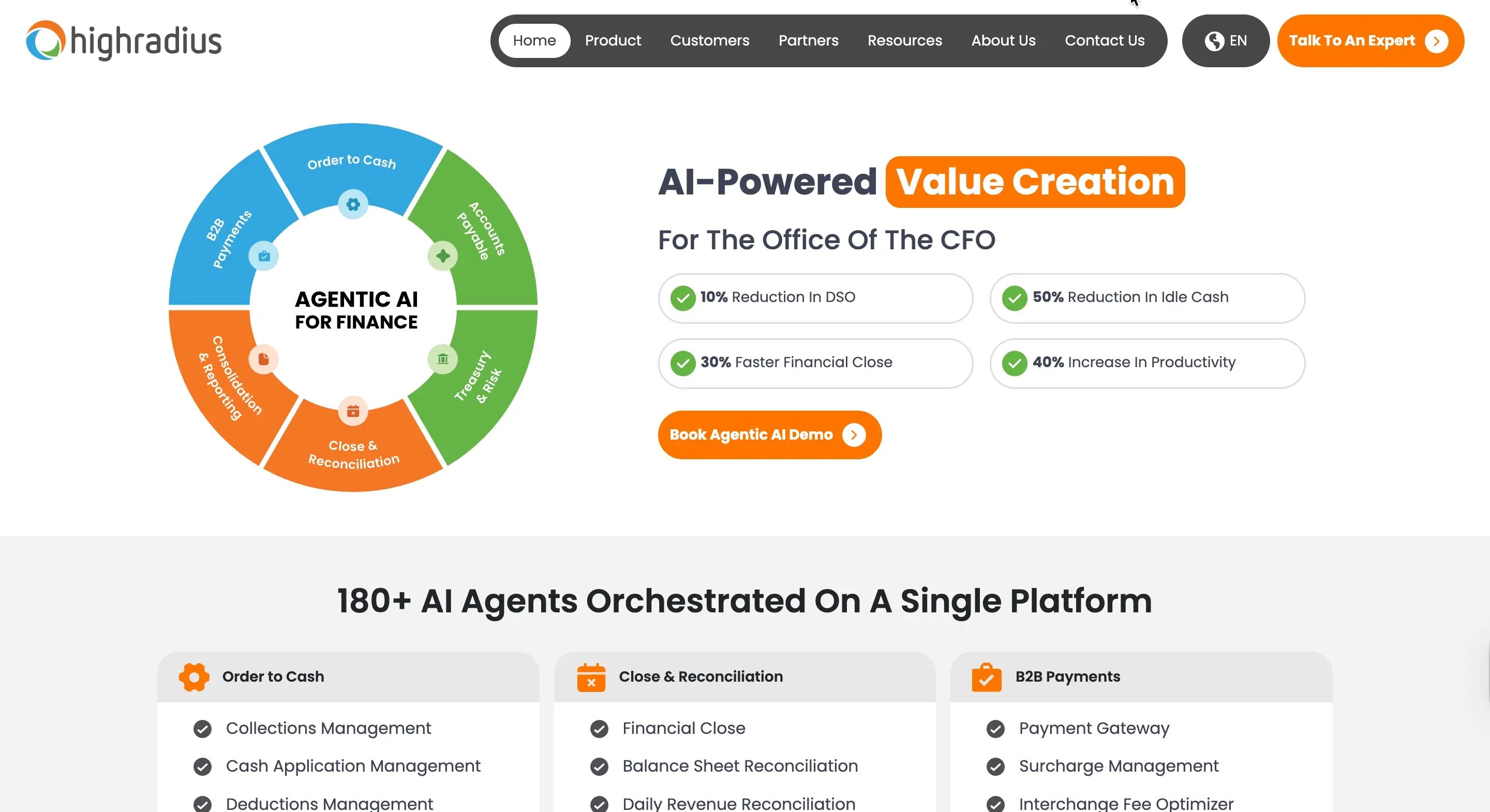

2. Highradius

Best for: Large enterprises with high invoice volumes that need AI-driven collections automation at scale across complex ERP environments.

HighRadius is built for enterprises where the collections problem is not a lack of reminders but a lack of capacity to work every account at scale. Its AI prioritizes daily worklists, automates outreach for long-tail accounts, and handles huge volume invoice uploads which is work that simply cannot be done manually at volume. The trade-off is a long average implementation period and enterprise-level cost. For businesses below $500M in revenue, it is unlikely to be the right fit.

It helps prevent invoices from aging, but if reminders stop working and debt becomes difficult, there is no integrated recovery service leaving the team to decide what happens next.

Key features

AI-powered worklist prioritization

HighRadius uses AI agents to rank overdue accounts by recovery likelihood, revenue at risk, and customer behavior. The system generates a personalized daily worklist for each team member, directing effort toward the highest-priority accounts.

Multi-channel outreach with in-app calling

Collections teams can make outbound calls directly inside the platform, with AI generating talking points beforehand and drafting follow-up notes afterward. Automated dunning emails run in parallel for long-tail accounts, so high-volume portfolios get consistent coverage without needing more staff.

Collection agency integration

When internal chasing reaches its limit, HighRadius connects directly to external collection agencies from within the platform. You can escalate accounts without manual handoff, and agency activity stays visible inside the same system.

Dispute prevention and management

AI agents flag invoices that show early signals of a dispute, mismatched POs, quantity discrepancies, missing proof of delivery before the customer raises a formal claim. That reduces the volume of disputes that would otherwise delay payment and require manual resolution.

Pros

It handles scale that mid-market tools cannot, enterprises processing tens of thousands of invoices monthly get genuine automation depth, not just reminder scheduling. Proven at 1,000+ companies with documented outcomes including 20% reduction in past dues and 30% productivity gains.

Cons

Onboarding and implementation takes a long period of time, which makes it a poor fit for businesses that need relief quickly. Customer support responsiveness is a recurring complaint in reviews, and customization can be slow once the platform is live.

Pricing

Custom quote-based only. No public pricing is available and evaluation begins through a demo request.

Reviews

Highradius Accounts Receivable has a rating of 4.4 from 13 reviews on Capterra. Users generally rate it highly for ease of use, visibility, and payment experience.

3. Paidnice

Best for: Small businesses using Xero or QuickBooks that want to automate reminders, late fees, and statements without managing a complex AR platform.

Paidnice removes the manual grind of following up on overdue invoices for small businesses already inside Xero or QuickBooks. Rather than a full AR platform, it's designed to be the automation layer sitting on top of an accounting system small teams are already using. So reminders go out consistently, late fees apply automatically, and statements land on schedule without anyone manually managing the process.

For businesses where chasing is consuming significant time and late fees are being missed, Paidnice offers a fast, affordable entry point.

Once customers stop responding to reminders, though, there is no escalation path, no human collections layer, and no visibility tools to identify which accounts are most at risk. At that point, the business is back to deciding what to do next on its own.

Key features

Automated email and SMS reminders

Reminders go out on a schedule the business sets; before the due date, on the due date, and at defined intervals afterward.

Templates are customizable so they match the business's voice, and the system respects weekends and public holidays so reminders do not arrive at times that make the automation obvious. Both email and SMS are supported, giving two channels of reach without manual effort.

Automated late fees and interest charges

Late fees and interest charges apply automatically based on rules the business configures which is by customer type, contract, or invoice age. For businesses that were previously calculating late fees by hand, or not adding them at all, this is a meaningful time saving and a direct financial recovery tool.

Automated statements

Paidnice can automatically offer and apply early payment discounts, giving customers a financial incentive to pay before the due date. This is uncommon in lower-cost AR tools and addresses a different part of the collections problem which is reducing lateness before it starts rather than chasing it afterward.

Prompt payment discounts

Paidnice can automatically offer and apply early payment discounts, giving customers a financial incentive to pay before the due date rather than after it. This is genuinely uncommon in lower-cost AR tools and addresses a different part of the collections problem.

Branded customer portal

Customers can access their invoices and payment options through a branded portal. However, the competitor data confirms this does not include self-serve invoice access in the fuller sense.

Pros

Extremely easy to set up inside Xero or QuickBooks. Customer support is consistently praised across reviews as responsive and hands-on during onboarding.

Cons

Paidnice is a Tier 1 tool only. There is no multi-stage escalation, no email inbox integration, no promise-to-pay tracking, no credit monitoring, and no integrated collections service. When reminders stop working, there is no next step built into the platform. It focuses mainly on Xero and QuickBooks integration, although businesses can build custom API integrations.

Pricing

Publicly available tiered subscription pricing starting. A free trial is available.

Reviews

Paidnice holds 4.9 out of 5 from 10 reviews on Capterra. The review base is small but consistently positive. The most repeated themes are time savings on late fee management, ease of integration with Xero, and the quality of customer support during setup.

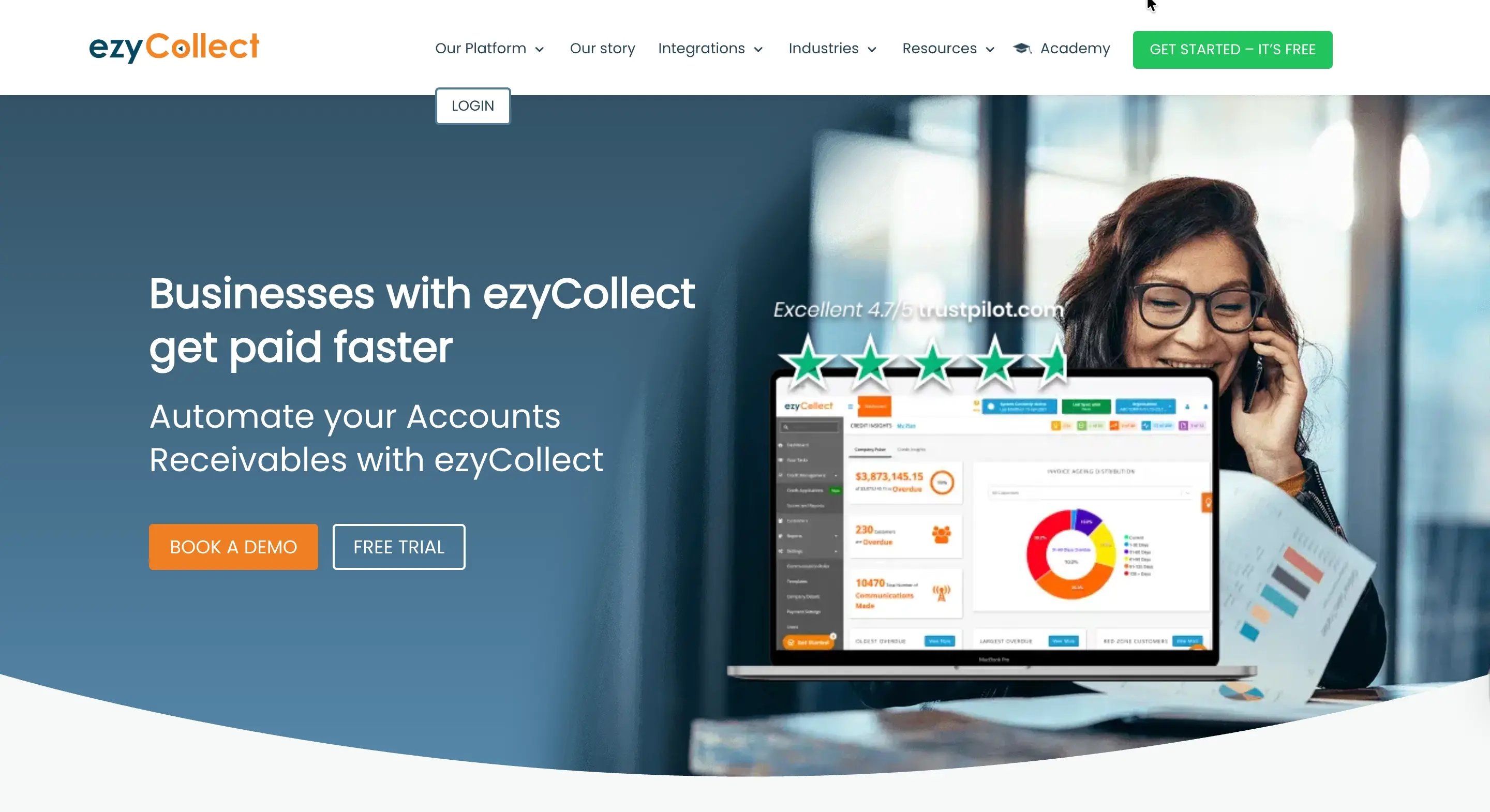

4. EzyCollect

Best for: Wholesalers, manufacturers, and construction firms in Australia and New Zealand that want AR automation combined with credit risk intelligence and a direct path to third-party debt collection.

EzyCollect is built around a specific problem that industries like wholesale, distribution, and construction face more acutely than most: the customer who looked creditworthy at onboarding is now paying everyone else on time but becoming unresponsive.

Most AR tools have no way to surface that distinction. EzyCollect does, by combining automated collections with live credit intelligence powered by illion, so the business can see whether a customer's financial position is deteriorating before the invoice ages into a write-off.

That combination of early-stage risk screening and multi-channel chasing handles most overdue debt before it becomes difficult. There is also a direct escalation path to third-party debt collection when reminders stop working. What sits in the middle is thinner. There is no outsourced credit control layer and no human follow-up stage for accounts that go quiet.

Key features

Credit Insights powered by illion

EzyCollect pulls live credit data from illion, one of Australia's credit bureaus, and overlays it against the business's own debtor records. The result is a risk-ranked view of the entire debtor list, not just who is late paying you, but who is showing deteriorating payment behavior across the wider market. High-risk debtors can be added to a near real-time monitoring service, with fortnightly risk reports sent to the inbox automatically.

Automated multi-channel reminders

EzyCollect sends email, SMS, and paper letters across configurable chase schedules, with call reminders for accounts that need manual follow-up. Templates are customizable and domain verification is supported, so reminders go out from the business's own email rather than a third-party domain.

One limitation is the platform does not restrict chasing to weekdays or exclude public holidays, which means automated messages can arrive at times that make the process feel impersonal.

SimplyPaid payment portal with Installment support

The SimplyPaid portal allows customers to view invoices, pay by multiple methods, part-pay, or arrange an installment plan directly without contacting the business. Automatic payment reconciliation writes back to the ERP, removing manual matching.

For construction and wholesale businesses where structured payment arrangements are common, this is more useful than a standard "click to pay" link.

Digital credit applications

Businesses can send customizable online credit application forms to new trade customers, replacing paper-based or PDF processes. Combined with Credit Insights, this gives the business a credit risk picture before the first invoice is issued rather than after the first one goes unpaid.

Pros

The credit intelligence layer is genuinely differentiated. Most AR tools in this category offer no view of how a customer is paying other suppliers, only how they are paying you.

Cons

No weekend or public holiday scheduling control. Without weekend or public holiday scheduling controls, reminders can arrive at times that feel impersonal, which matters for businesses where relationship tone is important. There is no outsourced credit control service and no human-led mid-stage escalation, making it weaker at Tier 2.

Pricing

Pricing is not publicly listed and is tailored based on business size, features required, and invoice volume.

Reviews

EzyCollect holds a 4.9 out of 12 reviews on Capterra, with implementation averaging under one month. The most consistent themes are time savings on manual chasing, improved cash flow visibility, and ease of integration with MYOB and Xero.

5. Payt

Best for: European SMEs and mid-market businesses that want automated AR with a structured pre-collection escalation step built in, without immediately handing debt to an external agency.

Payt is built around a problem that most AR tools sidestep: what happens between a reminder that goes unanswered and the decision to send an account to a collections agency.

Most tools leave that gap empty, but Payt fills it with SmartCollect: a structured pre-collection process that sits inside the platform, lets the business apply statutory penalty charges, and resolves an average of 65% of outstanding invoices without external agency involvement.

It is one of the few platforms that handles the gap between reminders and agency escalation through a built-in mechanism rather than leaving the business to figure it out. The limitation is that SmartCollect is still an automated process.

There is no human follow-up layer, and for accounts where automation has already failed, the next step is still a bailiff or external agency.

Key features

Automated follow-up from first invoice to final demand

The automation starts the moment an invoice goes unpaid and continues through to the final demand notice without manual intervention. Reminders go out by email, SMS, and paper letter.

The platform claims up to 80% time savings on follow-up and invoices paid 30–50% faster as a result of consistent, frictionless chasing. The process is fully visible and controllable as the business can pause, modify, or override at any point.

SmartCollect: Pre-collection escalation

When reminders have run their course and an invoice remains unpaid, SmartCollect adds a formal intermediate step before external debt collection. It applies legally permitted penalty charges (between €40 and €6,775 under Dutch law), continues automated customer-friendly communication, and resolves approximately 65% of cases in-house.

The business retains full control over how penalty charges are applied and they can be kept as revenue or waived to preserve the customer relationship.

AI payment prediction and automated calling

Payt's AI module analyses historical payment behavior to predict when an invoice is likely to be paid, allowing the business to prioritize action on high-risk accounts and adjust reminder timing accordingly.

A separate AI calling feature automatically phones customers when invoices appear to have landed in spam. The AI assistant helps the customer locate the email, assists with whitelisting, and logs call notes directly in the dashboard.

Smart payment plans

When a customer cannot pay in full, Payt allows payment plans to be initiated by either the business or the customer. A minimum payment amount is set and all subsequent follow-up is automated, just as it is for standard invoices. This is positioned explicitly as an alternative to starting a collections process. This helps preserve the customer relationship while still recovering the debt in installments.

Pros

SmartCollect is a genuinely differentiated feature. It is an in-house pre-collection mechanism that reduces external agency usage significantly while keeping penalty charges within the business. Payt handles volume at scale, with 1.5 million invoices processed monthly across the platform.

Cons

Payt has no email inbox integration, meaning customer replies to reminders are not captured inside the platform — the business still has to manage incoming responses separately.

There is no escalated sender or recipient functionality, no promise-to-pay tracking, and no configurable reminder scheduling around weekends or public holidays, which means automated messages can arrive at times that make the process feel impersonal.

Pricing

Publicly listed and tiered by invoice volume. A larger volume invoice is available on request. Monthly cancellation with no lock-in period.

Reviews

Payt holds a Trustscore of 4.6 from 1,231 reviews on Trustpilot. The volume of reviews is the largest of any tool on this list and reflects a long-established customer base, primarily in the Netherlands and broader European market. Recurring themes in positive reviews are time savings on manual chasing, the completeness of the automated process from invoice to final demand, and the quality of support during setup.

How to choose the right receivables management software for your business

|

Situation |

Recommended tier |

Best-fit solutions |

|

DSO 15 to 90 days. Invoices overdue but recoverable. Relationships still matter. |

Tier 1: Software automation |

Chaser, Paidnice, EzyCollect, HighRadius (enterprise only) |

|

DSO 90 to 120+ days. Customers are going silent. Relationships are still worth preserving if possible. |

Tier 2: Hybrid or pre-collection |

Chaser, Payt |

|

DSO 365+ days. Refusal to pay. The relationship is already gone. |

Tier 3: Agency or legal route |

Chaser collections, EzyCollect agency escalation, traditional RMS |

Start with debt severity. The tier table above is the fastest way to narrow the list. Most tools here are Tier 1 only, and only Chaser covers all three tiers in one platform.

From there, match the platform to the specific operational problem:

Aged debt with customers going silent → Chaser

Pre-collection escalation without an external agency → Payt

Credit risk screening before debt forms → EzyCollect

Late fees and statement automation for small teams → Paidnice

Enterprise-scale collections across complex ERP environments → HighRadius

If the business needs relief within 30 to 60 days, prioritize platforms with fast onboarding. Chaser and Paidnice are among the quickest to value. Payt's SmartCollect can activate on individual cases as soon as the platform is live.

The final test is always the same: run it against real invoices, real reminder flows, and the actual accounting system in place. A tool that looks polished in a demo but adds admin in practice is not a solution.

Final recommendation

For most mid-market businesses searching for receivable management services because debt is aging and the AR team is overwhelmed, Chaser covers the widest range of scenarios from early-stage automation through to integrated collections.

It is the only platform on this list that covers all three tiers. It automates early-stage chasing, adds a relationship-preserving human layer when customers go quiet, and provides integrated collections when recovery is needed. That means one system can do the work that usually gets split between spreadsheets, reminder tools, and outside agencies.

If the business cares more about prevention than recovery and wants a structured in-house escalation step before involving any external party, Payt is worth a closer look. If credit risk screening is the top priority, EzyCollect deserves a closer look.

If the business is small, already on Xero or QuickBooks, and simply wants consistent reminders and automatic late fees without a complex platform, Paidnice is the most accessible starting point.